Generics in Specialty: “The Future Ain’t What It Used to Be”

By subscribing, you sent consent to receive SMS or MMS messages from The Remedy Group. To opt out of our text messaging program, send the word STOP to 503-753-9029 at any time. View our Terms of Service and Privacy Policy. Msg & Data rates may apply. Message frequency varies.

February 14, 2018

By admin

After experiencing the shift toward generic acceptance in retail pharmacy, specialty pharmacy providers (SPPs) rightfully longed for a future buoyed by generics in the specialty channel. After all, generics provide the same clinical benefits as their innovator products, but at a lower cost and with a potentially higher margin. Although seemingly illogical, it is important to remember that other stakeholders may not share this sentiment. Patients, providers, and even some payers often prefer a more expensive branded product in lieu of a clinically equivalent generic product.

Generics in the specialty channel currently include medications for multiple sclerosis (MS), oncology, HIV, and transplantation, among others. The widespread acceptance of these therapies is a high-stakes matter, as SPPs that encourage rapid adoption of new specialty generics are poised to wield a distinct competitive advantage. This advantage will likely be long-lived, since generics can be viewed as a litmus test for the tidal wave of biosimilar products in the pipeline. With help from the late, great Yogi Berra—the master of paradoxical half-truths—the challenges facing SPPs in persuading other stakeholders to embrace generics are explored below.

Generic Inferiority: “It’s Like Déjà Vu All Over Again”

Once an incomprehensible proposition, generic drug products have become a cornerstone of the retail pharmacy industry. Although patients and providers may still meet newly approved generic medications with friction, these stakeholders now largely accept the clinical equivalence of a generic to its branded counterpart. The long-held beliefs of clinical inferiority and increased incidence of adverse effects—based on a lack of controlled clinical trials—have been squashed based on years of empirical evidence to the contrary. Patients who would previously eschew the thought of using a nonbranded medication now actively request treatments with generic availability.

To those who practiced retail pharmacy during the early days of generic infiltration, the paradigm shift described above was considered unfathomable. Today, SPPs are experiencing a similar systematic resistance to newly approved generics. Although this resistance is grounded in the same concerns regarding efficacy and adverse events that were seen with retail products, the specialty populations involved further complicate the substitution of generics.

Patients and prescribers needing specialty therapies for conditions such as cancer, MS, and HIV vividly recall the malaise and suffering caused by these conditions before treatment was initiated. Understandably, these fears make switching to a generic version of a life-sustaining drug a significantly more daunting proposal than generic substitution for an asymptomatic condition, such as high blood pressure or cholesterol.

However, both the unstoppable force that is rising drug prices and the immovable object of downward price pressures point to generics as a mechanism to achieve the lofty goal of decreasing costs while maintaining quality. Just as patient-centric innovations originally galvanized the specialty channel, SPPs must innovate to increase the utilization of these clinically equivalent, lower-cost therapies. These innovations, and the corresponding high-touch services that differentiate SPPs, must be a collaboration among all stakeholders to address comparative clinical efficacy and cost, which are the primary concerns a patient or provider may raise over generic substitution.

Clinical Equivalence: “90% is Mental, the Other Half is Physical”

The primary concern with any generic product is comparative safety and efficacy. After all, patients successfully taking a branded product hesitate to fix that which is not broken. These generic products receive regulatory approval via an Abbreviated New Drug Application (ANDA), which piggybacks on the demonstrated safety and efficacy of the innovator product. The ANDA requires the filing manufacturer to demonstrate the ability to produce the identical active pharmaceutical ingredient and acceptable bioavailability of the said ingredient. While these approvals do not require controlled clinical trials, their absence is not new. Generic approvals have occurred for decades under these circumstances, and practicing medical professionals have grown comfortable with this reality.

SPPs must not take for granted their knowledge of the positive history of generics, because what seems like common knowledge is unknown to patients and many providers. In addition to leveraging the track record of generics, specialty pharmacy representatives are able to combat resistance, in a more effective way, by genuinely and empathetically listening to the concerns of the patient and provider. By addressing concerns in this way, SPPs can alleviate the emotional distress that may accompany a change to a generic product.

It is important to not discount the importance of high-touch patient care. Remember, these patients and providers are not afflicted with, and providing treatment for, asymptomatic disease states. These patients received a devastating diagnosis after weeks, months, or years of searching for answers and relief. Now that they are further along in their treatment journey, the possibility of that fear and suffering that they experienced prior to receiving their diagnosis could recurr is more than unpalatable. The only way to identify, and subsequently resolve, emotional resistance to generic substitution is to explore the patient-provided reasons and compassionately work to resolve the concerns.

Cost Pressures: “A Nickel Ain’t Worth a Dime Anymore”

After clinical concerns, out-of-pocket expense is often the next most important factor in the decision-making process. One would expect the generic value proposition—clinical equivalence at a lower cost—to lead to an overwhelming uptake of generic products. After all, cost savings ultimately caused the paradigm shift toward the adoption of generic medications for the treatment of chronic conditions in the retail space.

For instance, atorvastatin largely replaced Lipitor shortly after entering the market. The broad availability of agents to treat hyperlipidemia, both branded and generic, allowed third-party payers to align patient cost share to effectively incentivize generic conversion. With a multisource generic available at a 90% discount of its branded counterpart, even manufacturer co-pay reduction programs were unable to mitigate the erosion of the branded market share.

Unfortunately, the cost differential between brand name and generic products is not so straightforward in the specialty channel. With smaller patient populations relative to nonspecialty conditions, a generic manufacturer needs greater revenues to offset its fixed costs, effectively absorbing some of the discount traditionally passed on to payers and patients. Combine this reality with the newfound savvy of branded manufacturers, via hub-commissioned benefits investigations and aggressive co-pay reduction programs, and branded manufacturers have eroded the cost advantage previously enjoyed by their generic competitors.

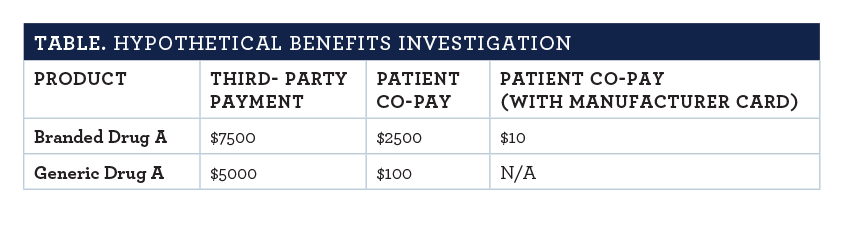

Consider the hypothetical patient in the TABLE.

This patient has achieved remission to a life-threatening diagnosis while receiving Branded Drug A. Now that Branded Drug A has lost its patent protection, the insurance has structured cost sharing to encourage the switch to Generic Drug A.

The plan design change implemented when generic competition reached the market was crafted to have patients requesting generics—as many now do in the retail space. The aforementioned branded manufacturer savvy is well noted in the table’s rightmost column. By subsidizing patient cost, the firm that is marketing the branded product wisely sacrifices a marginal amount of revenue to maintain market share. In this scenario that plagues generic substitution in specialty pharmacies all too often, few patients will opt to pay significantly more out of pocket to switch to a generic—a name that wrongly infers inferiority.

Just as branded pharmaceutical firms evolved to compete with generic manufacturers, the generic companies must pivot to act more like branded distributors. Innovative generic shops, such as SUN Pharmaceuticals, are doing exactly that. SUN curates a generic co-pay reduction program for imatinib, while Sandoz and Mayne Pharma offer out-of-pocket reductions for Glatopa and dofetilide, respectively. These programs do not fully restore the out-of-pocket cost benefit traditionally associated with generics, but they eliminate any artificial cost advantage crafted by manufacturer programs.

Content courtesy of Specialty Pharmacy Times